So usually I write this at the same time as my annual forecast but hey, stuff happens and this sort of fell along the back burner. So at the risk of the usual hindsight is 20-20 comments, I’m publishing this anyway, six months late. (better late than never right). That being said, I am of the view that we are only NOW really going into the year of the Monkey, having experienced a very prolonged conversion of energies from the year of the Goat to the year of the Monkey. So this post, whilst late, is arguably not THAT late.

The usual disclaimers: economic forecasts are difficult and complex creatures, and you should not rely on the information here for investing purposes since it is being produced here for strictly academic discussion. If you do, you hereby acknowledge that the risk is your own, and all your actions are your own.

As always, we begin with the chart of the year.

2016 BaZi chart

So, the cold hard elemental analysis was already done here, but the main elemental takeaway is this:

- SUPER STRONG Water (also means, highly competitive water)

- Metal Wood Clash as a Theme (how does this play out economically?)

- Fire faced with Rob Wealth Stars

Now, how do we translate this in to economic theory? And for those who read my forecast in the past, you will note that I’m dispensing with the sectoral analysis this year because I’m not sure it makes sense (but may return to it)

Strong Water: Commentary

Firstly, water invariably denotes volatility. So strong water here in the year naturally denotes tremendous volatility. What is volatility? One would perhaps define this as ‘reactiveness’ – any kind of gyration prompt a reaction. So we can say that we should expect the markets (and the participants in global markets) to be jittery and easily spooked or moved to act, sometimes possibly without reason or rationale…as my next point notes…

In BaZi, Water also represents emotion. Depending on your economic POV, you either perceive gyrations in the stock market as an indication of rational logic (people are simply doing what they would do what confronted with uncertainty) or as an indication of emotional reaction (after all, automated algorithms that power many trades are still done by human beings, based on parameters by human beings, and one must not ignore the fact that traders do think like herds). However, in BaZi, Water also equals emotion. Which means that it is largely emotion (“Fear” is an emotion no?) that is driving the volatility.

In theory, super strong water should be good for the property sector. This is because Water is the wealth of Earth, which represents the property sector. So property is flush with wealth – surely we should all be seeing good outcomes from this?

I think the first thing that I’ve realised from doing these forecasts is that one must not look at the current year as the OUTCOME per se, but rather, the CULMINATION of actions. It is a bit like how we look at a person’s BaZi. Oftentimes, when we forecast a person’s destiny for the year, we have to take into account, what they did the year before. This is because outcomes are cumulative as well as immediate. So similarly, when we look at the performance of a given economic sector, it makes sense to posit that the year’s forecast should represent both current and cumulative outcomes.

So back to the property sector seeing tremendous wealth. On the one hand, this can be said to be reflected in the fact that house prices and real estate has actually appreciated significantly, in many parts of the world. (see Bloomberg’s story on how two Swedish sisters have become billionaires just because property prices in Sweden have appreciated). But obviously, this benefits companies with vast real estate holdings, rather than those selling property arguably. Further, there is some argument that elementally, property development should not be confused with property holding – property holding, vis a vis trusts, REITs and other forms of holdings, is pure earth – property development has Wood mixed into the equation. Construction would also be considered Earth and by and large, appears to be doing reasonably well).

As for the argument that property developers don’t seem to be doing well this year, comparatively, again, one must deploy the cumulative element. I think many property developers are likely to see their earnings eroded in the immediate future, but what they are doing now is collecting the cash that comes from their previous endeavours. They aren’t selling NOW, but they are reaping the profits or rewards from their sales previously. (for example, EcoWorld in MY reported surge in revenue, as did UEM Sunrise).

Who then is feeling the pinch of the sluggish property market? It’s the small owners and the agents. The lowest in the pecking order and those with the least holding power. Those who are relying on the year to generate results rather than those who can rely on a cumulative effect or culminate effect.

Metal-Wood Clash: Commentary

This can be interpreted both globally (in the context of the clash) and individually, in the context of how the Metal and Wood industries do in 2016. Brief recap: Metal (manufacturing, automobiles, minerals, metals, FX, equities, money markets generally) and Wood (commodities, agriculture, education, timber, forestry).

Wood presents an interesting case – last year, I wrote this:

The Resource Star for Wood industries is Water, and it is weak in 2015. This would suggest that hardier crops, rather than those sensitive to rain or drought, would perform better than crops with tremendous vulnerability to water issues (such as rice). This of course gives rise to a unique situation where commodities traders (who make money from futures or hedging of commodities) will do well, whereas producing countries that rely on agriculture for income may find themselves either blossoming or blighted, depending on their crop mix. Weakness of water in 2015 clearly indicates drought or water related problems, which affects harvest for countries with less sophisticated agricultural methods.

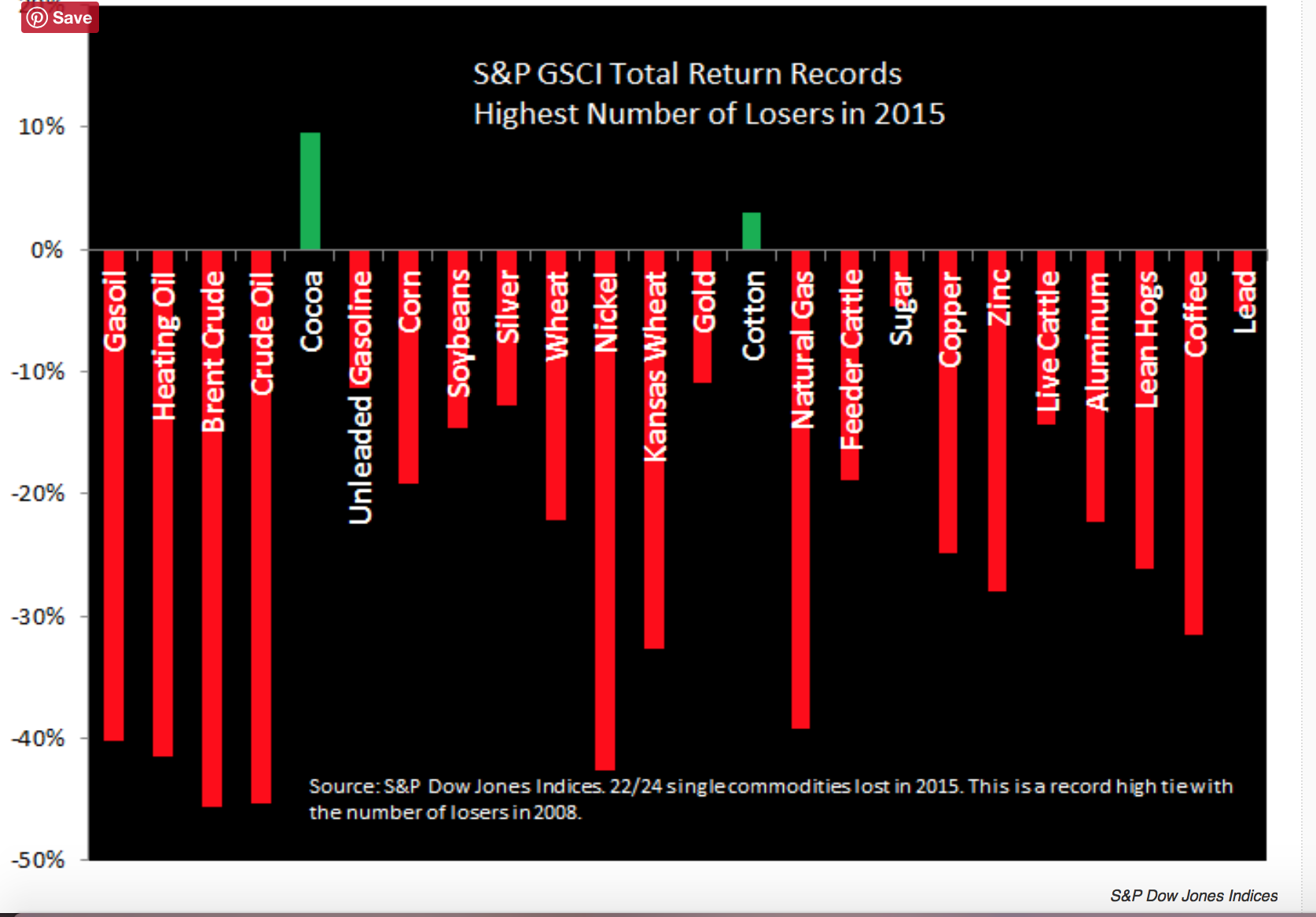

When I checked in mid 2015, there was nothing to indicate that it was an issue but now, the news is creeping out. Business Insider declared “2015 was a bloodbath for commodities”. (chart stolen from them too!) And aside from Cocoa, which did perform, Vanilla beans are also rising in price.

Of course, this year, strong water corresponds with concerns that after El Nino last year (too hot – per the chart, which did not have enough water), this year, we must worry about La Nina (too much water).

When the Shen-Zi-Chen kicking in during August, and peaking in December (extending as far as April 2017), there is no doubt we will have La Nina and this will create huge problems for the commodities industry. Yi is in Graveyard and Jia is chopped by Geng – this can be possibly interpreted to mean large trees (timber, rubber, palm oil) will be negatively affected (possibly chopped down due to disease or just poor growth or premature harvesting) whilst commodities that grow in the ground may potentially be less affected (soybean, potatoes) whilst those that are small but above ground will be washed away (read: flooding issues).

Since Earth is considered weak in this chart, commodities won’t be profitable or do well this year because there is no wealth for Wood. For other wood industries like education, property development, publishing, the lack of Earth this year coupled with the strong Metal means no revenues despite mounting regulations or forced M&A.. However, recalling that outcomes are cumulative, we need to know next year’s chart to figure out if for example, jumping into such industries now (whilst prices are hammered for example – NOTE: THIS IS NOT INVESTMENT ADVICE) is a good idea.

Metal presents a tricky proposition in 2016. On the surface, it LOOKS strong, being rooted in the Rooster and the Monkey in the year. However, with so much water in the mix, it’s open to question if Metal can actually chop the wet wood in 2016. Translating it into economic speak, we are looking at clear and present opportunities for Metal industries to make money but there is a hold back caused by possibly uncertain approach in the industry (long or short, contrarian or strategic). As Geng seems to be in a better position than Xin in 2016, we should expect large Metal (industrial equipment vs precision manufacturing, SUVs vs sports cars, international banks vs boutique banks) to perform better than small Metal. In terms of FX and commodities, I don’t see gold necessarily doing that well since Xin = Gold and it is only Direct Wealth for Gold this year (Jia Wood, since the Yi Wood is in graveyard, suggesting profits that cannot be extracted). Again, FX and equities will have the problem of the volatility (caused by the water) and possibly, the lack of any real clarity in terms of strategy overall in the market.

Rob Wealth in the Fire Sector: Commentary

So it’s obviously going to be hindsight is 20-20 to say oil has sucked balls big time this year. Last year, I wrote this:

However, it seems one should not be too optimistic of the price of oil rebounding significantly according to the BaZi of the year for two reasons: firstly, the final pillar of 2015 is 甲午 which is the annual pillar for 2014 (when oil prices started to slip), secondly, the final pillar of the year is strong fire consuming its own resource, suggesting that the industry must continue to operate in survivalism mode rather than prosperity mode.

Volatility (water) has obviously heavily influenced oil prices as well, which seem to create all kinds of reactions even when all they do is budge by a dollar or so. But for the most part in 2016, oil prices haven’t moved much.

We may see some progress during the Autumn season (August, September, October) since these are the Metal months and Fire (which represents the oil industry/energy sector) should see some improvement financially. HOWEVER, as August and September both present with Fire (Bing Shen in August, Ding You in September), we should not really expect the prices to substantially increase since the Companion Star is present each month. That suggests that there will be heavy profit taking every time the prices moves even a little, and continuing cannibalism, price wars, intensified competition, in the industry, even as prices increase moderately. Again, we need to see what 2017 holds for the industry if one is to determine if it is wise to invest in oil sectors at this stage. However, as we move closer into the strong Water months (November, December, January and of course, April 2017) we should see volatility in the markets shake the oil sector even more (remember, water is 7 Killings/Direct Officer to Fire so it will be the first recipient of volatility since volatility creates pressure and 7K represents pressure/stress) as companies come under intense performance pressure or scrutiny.

Goat to Monkey transition: disruption and the ending of the old order

One of the topics of discussion amongst metaphysics enthusiasts has been the unnaturally long transition out of Goat (lasting all the way till July 2016) and the prolonged period of intermingling of the Goat-Monkey energies. The reasons for this phenomenon can in my humble theorising, be attributed to the following possibilities:

- Season change is more drastic from Goat to Monkey vs Dragon to Snake. Wood to Fire feels more natural than Fire to Metal. Temperature change is also more drastic. That is why the changeover of the energies has been more chaotic and also, less predictable

- Goat is Graveyard, Monkey is Growth. Essentially the energies go in two opposite directions – one represents decline, the other represents movement forward. One is the old world, resisting the end of it’s way of doing things, the other is the new world, eager to be birthed and make a difference. When the old must make way for the new, it’s never an easy fight – best illustrated by the classic battle of old and new in 2015/2016: Uber vs everyone else, AirBnB vs everyone else. Politically we also see this – the rise of Donald Trump arguably represents an attempt to fight back against the old order, the elite, the old way of doing things. Earth-centric Earthly Branches meanwhile tend to represent procrastination, decay, slowness, graduated decline – is it any wonder the Goat has resisted slaughter, even as the Monkey demands it’s day?

Way back in 2008, I theorised that everything that related to the 2008-2009 financial crisis would only reach full circle once the cycle went back to the Growth Star. So if we take 2008 as the start point, then the Growth Earthly Branch is Monkey (Rat => Dragon => Monkey). If we take 2009 as the start point, then the Growth point is Snake (Ox => Snake). There are many economists who believe that we still haven’t actually recovered from 2008, despite all the positive ra-raing. If we follow this argument, then we are, in the year of the Monkey, at the cusp of a new cycle of moving forward. But first, the old order…must die!

Hi BaziQueen,

I have problem understand this sentence below…

So if we take 2008 as the start point, then the Growth Earthly Branch is Monkey (Rat => Dragon => Monkey). If we take 2009 as the start point, then the Growth point is Snake (Ox => Snake).

Could you clarify further?

Thanks

If you don’t know the Three Harmony Frame, then it won’t make sense.

i know monkey is autumn season and monkey is also a growth star

i also know SHEN ZI CHEN form water frame

i just do not understand why you put (Rat => Dragon => Monkey)?

i also know snake is summer season and also is a growth star.

i also do not understand (Ox => Snake).

I would appreciate your reply.

The key art to master in BaZi is the theory of connectedness. We look for patterns. And patterns emerge from the frames.

I also don’t understand what you don’t understand. So maybe it’s not the right time for you to figure this out yet.

Hi BaziQueen,

Please let me know if you can ship your video classes to Bucharest, Romania

Thank you!

My apologies for the late reply. I can ship anywhere DHL ships to. Please email me at bazibuzz@gmail.com for more details.